FFF Insight 7 - CGT Changes for Farming Families: What the New $10 Million Threshold Means

Jun 23, 2026

A Positive Step Forward for Farm Succession Planning

For many farming families, succession planning is not just about transferring assets. It is about preserving a legacy, protecting family relationships, and creating opportunities for future generations.

The Federal Government has announced a significant change that could create new planning opportunities for thousands of Australian farming families.

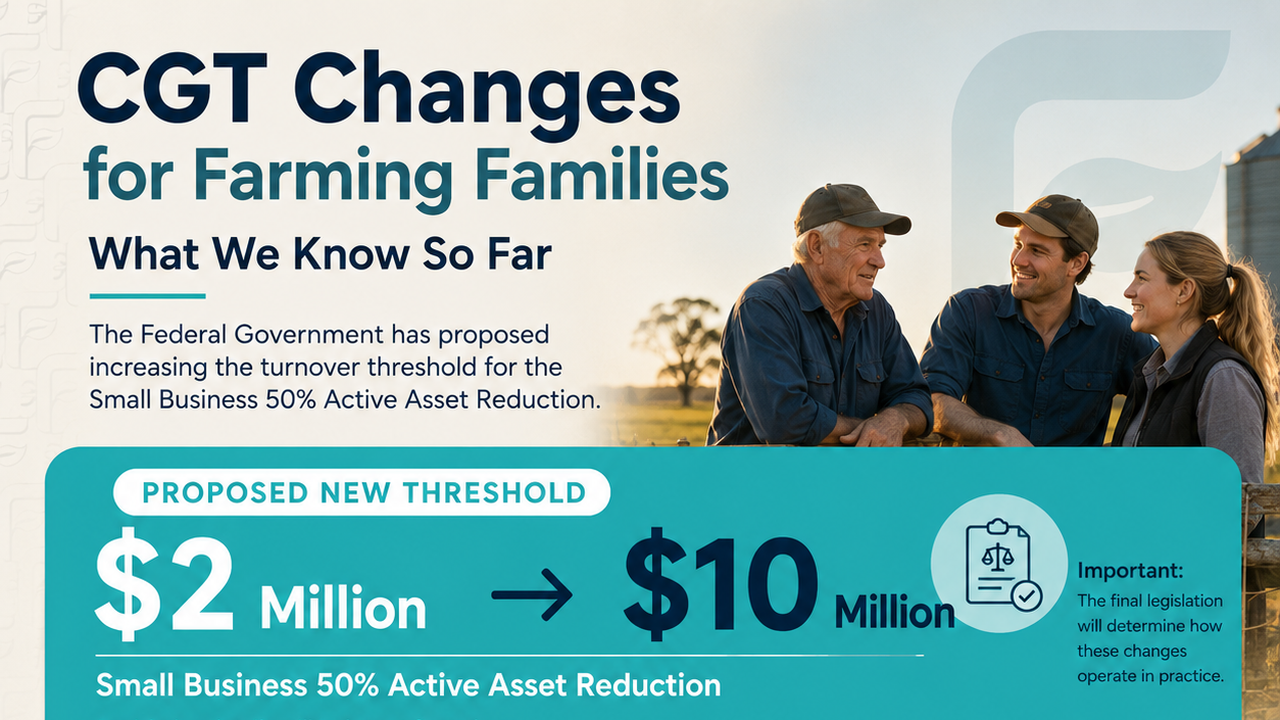

The turnover threshold for the Small Business 50% Active Asset Capital Gains Tax (CGT) Reduction is proposed to increase from $2 million to $10 million.

While that may sound like a technical tax change, the implications could be significant.

For years, many family farms have been too large to qualify for certain small business tax concessions, yet nowhere near large enough to be considered corporate enterprises. Rising commodity prices, inflation, increasing land values and larger farming operations have pushed many genuine family farms beyond thresholds that were established decades ago.

The proposed increase to $10 million is a welcome recognition that modern farming businesses have changed.

While we believe the threshold could ultimately be increased further to better reflect the scale of contemporary agriculture, this is an important step in the right direction.

Why This Matters

Many farming families spend decades building productive businesses that support multiple generations.

Eventually, every family faces important questions:

- How will ownership transition to the next generation?

- How can retirement be funded fairly?

- How can family relationships be protected during succession?

- How can unnecessary tax be minimised?

Capital Gains Tax often becomes one of the most significant considerations during succession planning.

The proposed expansion of access to the Small Business 50% Active Asset Reduction means many more farming families may potentially access valuable tax concessions when transferring, restructuring or ultimately selling business assets.

Understanding the Concession

The Small Business 50% Active Asset Reduction allows eligible businesses to reduce a capital gain by a further 50%.

Importantly, this concession sits within the broader Small Business CGT concession framework and has historically been one of the most commonly used concessions by farming families.

These concessions are commonly considered when:

- Succession plans are implemented

- Farm ownership structures are reviewed

- Assets are transferred between generations

- Retirement strategies are developed

- Business restructures occur

- Farm assets are sold

For many families, the availability of these concessions can materially influence succession outcomes.

An Important Detail: The Legislation Still Matters

While the headline announcement has generated considerable interest, the detailed legislation will ultimately determine how the changes operate in practice.

Based on the Government's announcement, the intention appears to be to retain the existing Small Business CGT concession framework while expanding access to the 50% Active Asset Reduction through the increased turnover threshold.

The final legislation will confirm exactly how the changes interact with the broader concession regime and existing eligibility requirements.

As always, families should avoid making major decisions based solely on headlines and instead seek advice on how the changes may apply to their specific circumstances.

What About Other Small Business CGT Concessions?

One of the questions being asked by advisers and business owners is how the proposed increase will interact with the broader Small Business CGT concession framework.

At this stage, the Government's announcement has focused specifically on expanding access to the 50% Active Asset Reduction.

Other important concessions remain in place, including:

- The Small Business 15-Year Exemption

- The Small Business Retirement Exemption

- The Small Business Rollover

Many farming families also qualify for Small Business CGT concessions through the Maximum Net Asset Value Test rather than the turnover test.

As more detail becomes available, advisers will be examining how these provisions interact and whether additional planning opportunities emerge for farming families.

Don't Forget What's Already Available

While much of the current discussion is focused on proposed changes to the Small Business CGT concessions, it is important not to overlook the opportunities that already exist today.

Many farming families are surprised to learn that valuable succession planning tools may already be available, including:

- The Small Business 15-Year Exemption

- The Small Business Retirement Exemption

- The Small Business Rollover

- The Maximum Net Asset Value Test

- The Small Business Restructure Rollover (SBRR) - $10m turnover threshold

In our experience, some of the most successful succession outcomes occur not because of a new tax concession, but because families understand and utilise the concessions and planning opportunities that are already available.

The proposed reforms are certainly welcome, but they should also serve as a reminder to review your current position and identify opportunities that may already exist.

While governments may change the rules, farming families can still control the controllable—the conversations, planning and decisions that shape the future of the farm.

The Bigger Opportunity

The real significance of this announcement is not simply the tax saving.

The real opportunity is the conversations it may encourage.

Too many farming families delay succession planning because it feels overwhelming, complicated or uncomfortable.

Yet waiting rarely makes the process easier.

The most successful transitions often occur when families start planning early, communicate openly and understand the options available to them.

This announcement may create opportunities that previously did not exist for some farming businesses.

It may also provide a timely reason for families to review succession plans that have not been revisited for many years.

Changes to tax legislation, business structures, land values and family circumstances can all affect whether an existing succession plan remains fit for purpose.

What Farming Families Should Consider

As legislation progresses, farming families may wish to review:

Succession Plans

Do existing plans still achieve the family's objectives?

Ownership Structures

Are current structures still appropriate for the next stage of the family's journey?

Retirement Planning

Will retiring generations have sufficient income and security?

Family Communication

Are expectations clearly understood between generations?

Future Opportunities

Could previously unavailable concessions now become accessible?

Every family's situation is unique, but understanding the potential opportunities early can provide greater flexibility when important decisions need to be made.

Preserve. Protect. Prosper.

At Future Farming Families, we believe every successful succession plan should focus on three priorities.

Preserve

Preserve the farm, the legacy, the opportunities and the wealth created through generations of hard work.

Protect

Protect family relationships, family values and family assets throughout the transition process.

Prosper

Create opportunities for future generations to thrive and continue building on what has been established before them.

This announcement represents a positive step towards helping more farming families achieve all three.

The Bottom Line

The proposed increase in the turnover threshold from $2 million to $10 million is a welcome and overdue recognition of the scale of modern farming businesses.

While the final legislative detail still needs to be confirmed, the reform has the potential to create new planning opportunities for many farming families who have previously been excluded from key CGT concessions.

Most importantly, it serves as a reminder that succession planning is not a one-off exercise.

As circumstances change, families should regularly review their plans to ensure they remain aligned with their goals, values and long-term vision for the future.

After all, the future of the farm is rarely determined by a single season.

It is shaped by the decisions families make today.

Want to Learn More?

Recent discussions around CGT concessions, trust structures and succession planning have created plenty of questions for farming families.

If you'd like a deeper understanding of the issues currently shaping farm succession planning, listen to:

Episode 7: CGT & Trust Changes Update – What Every Farming Family Needs to Know

In this episode, we explore:

- Proposed CGT changes and what they could mean for farming families

- Trust structures and succession considerations

- Common misconceptions surrounding tax and succession planning

- Practical considerations for families planning their future

Ready to Secure Your Family's Future?

Preserve the legacy. Protect what matters. Prosper together.

Future Farming Families helps farming families become Succession Ready by providing the guidance, tools and support needed to build a successful Succession Blueprint for the future.

Whether you're just starting the conversation or actively planning the transition, you'll gain access to practical resources, expert insights and a community of farming families committed to creating a stronger future.

Join the Future Farming Families waitlist today and receive complimentary access to the Family Legacy Project Workbook.

Join The Waitlist

Be sure to get on the waitlist to hear when our Foundations program goes live.

When you signup, we'll be sending you weekly emails with additional free content